1. How Investors Will Think About Your Valuation

As you go out to raise capital, you need to understand how investors will frame the price of your round and the ownership they will demand.

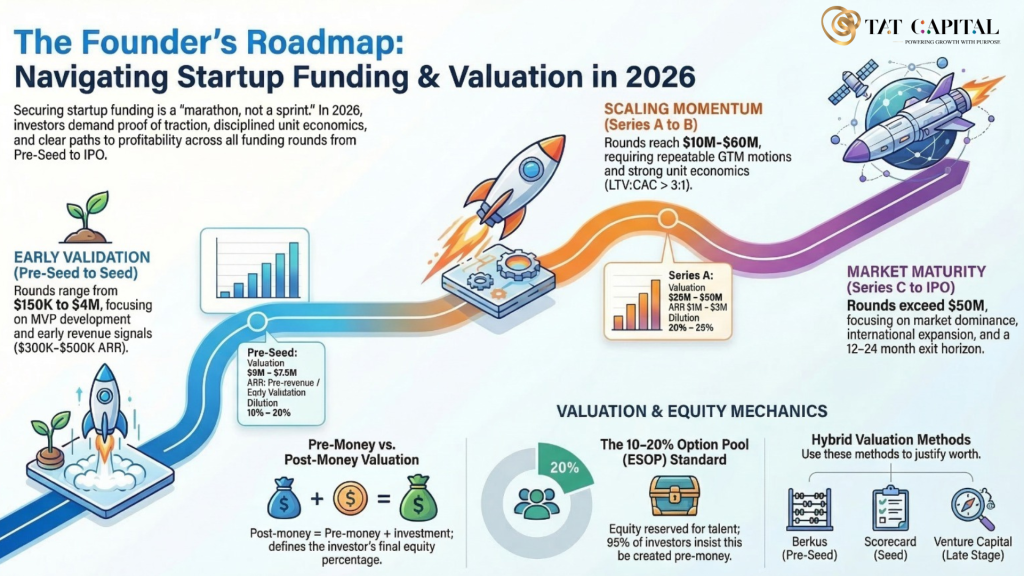

At its simplest, investors think in terms of pre-money and post-money valuation.

- Post-money valuation = Pre-money valuation + New investment amount.

- Equivalently, Post-money valuation = Investment amount / Equity % offered to investors.

If, for example, you raise 2 million at 10% dilution, investors are implicitly valuing your company at 20 million post-money and 18 million pre-money. As your banker, I want you to internalize that every negotiation on valuation is really a negotiation on how much of the company you are selling in this round.

For pre-revenue or very early businesses, sophisticated investors will often apply the Venture Capital Method: they estimate your exit value in 5–10 years and work backwards using their target multiple.

- Post-money today = Expected exit value / Target ROI.

- Pre-money today = Post-money − Investment amount.

2. How They Will Value an Early-Stage, Pre-Revenue Startup

Because you do not yet have a long financial history, investors lean heavily on qualitative signals and market potential rather than traditional metrics like EBITDA or cash flow.

You should expect them to focus on:

- Strength and completeness of the founding team.

- Size and urgency of the problem and market.

- Product progress (MVP, prototype, early users).

- Signs of early traction: waitlists, pilots, engagement metrics, even if revenues are small.

Many early-stage investors will swap financial metrics for operational benchmarks such as MAUs, retention, CAC, and conversion rates when comparing you to other companies. At this stage, valuation is often driven less by “intrinsic value” and more by target ownership and competitive deal dynamics.

You will also see investors use structured heuristics instead of complex financial models:

- Berkus Method: Attaches explicit dollar values to factors like your idea, prototype, team, strategic relationships, and early sales or rollout.

- Scorecard Method (Bill Payne): Starts from an average valuation for similar deals in your region and then adjusts up or down based on how you score on team, market size, product, competition, and go-to-market.

- Risk Factor Summation Method: Starts from a baseline valuation and then adds or subtracts value across risk dimensions such as technology, market, funding, competition, and regulation.

As your advisor, my guidance is to proactively shape the narrative and materials around these levers: showcase your team, quantify your market, highlight product milestones, and address key risks head-on.

3. Valuation Methods You Will Encounter

When you talk to investors, you will likely hear a mix of approaches. Being fluent in these will help you negotiate confidently.

Common methods for pre-revenue and early-revenue startups include:

- Berkus Method: Good for very early rounds; typically caps out around 2.5 million based on five qualitative factors. You can use this as a sanity check for very early valuations.

- Scorecard Method: Most useful when there is a clear, local benchmark for your sector; your job is to show why you should be scored above average on team, market, and product.

- Risk Factor Summation: Works like a structured risk memo; de-risking specific categories (e.g., regulatory, technology, funding) directly supports a higher valuation.

- Venture Capital Method: Forward-looking; investors “back-solve” what they can pay today given a target exit and required multiple.

- First Chicago Method: Scenario-based (upside, base, downside); more common with sophisticated funds or later rounds in uncertain markets.

- Cost-to-Duplicate: A conservative floor, based on what it would cost to recreate your product and assets from scratch, often used as a negotiating anchor by investors.

Traditional Discounted Cash Flow (DCF) analysis usually comes into play only once you have meaningful and somewhat predictable revenues (typically Series B and beyond). Before that, do not rely on DCF as your primary valuation justification; it will not be credible to institutional investors.

4. How Your Funding Journey Should Evolve

As your banker, I want you to think of fundraising as a staged journey, where each round has a clear objective, metric profile, and investor type. Aligning your story to these expectations will materially improve your odds of closing high-quality capital.

Seed: Prove Product–Market Fit

- Goal: Move from a validated idea to a working product with clear early adoption and product–market fit.

- Typical profile: Functional MVP, strong early user signals, many founders now target 300k–500k (sometimes up to 1.5 million) in ARR for a strong Seed in SaaS.

- Round size: Usually 2–4 million at 10–30 million pre-money valuations.

Your pitch here should emphasize the problem, your solution, early traction, and a credible plan to convert Seed capital into scalable revenue.

Series A: Scale a Repeatable GTM Engine

- Goal: Turn early traction into a repeatable, scalable go-to-market model.

- Typical profile: 1–3 million in ARR (some investors now look for 2–5 million), 15–20% monthly growth, and healthy unit economics (LTV/CAC).

- Round size and valuation: Roughly 10–20 million raised at 25–50 million pre-money valuations.

Here, investors will underwrite you on efficiency and repeatability rather than vision alone. You need tight cohort data, clear sales funnels, and evidence that each incremental dollar of spend can reliably generate revenue growth.

Series B: Accelerate Toward Market Leadership

- Goal: Scale aggressively, consolidate your category, and build organizational depth beyond the founders.

- Typical profile: 5–10 million in ARR (often higher for category leaders), NRR above 100%, strong burn multiple and a visible path to profitability.

- Round size and valuation: Often 20–60 million raised at 80–140 million valuations.

Your story now must shift from “this works” to “this can be the dominant winner.” Be prepared for deeper diligence into your metrics, organization, and governance.

Series C: Global Scale

- Goal: International expansion, new product lines, and strategic M&A.

- Typical profile: 20–50 million+ in ARR, near public-company governance standards, clear line of sight to an exit within a couple of years.

- Round size and valuation: 30–100 million raised at 100–500 million+ valuation.

At this stage, you are being underwritten as a pre-IPO asset. Your board composition, controls, audit readiness, and risk management will all matter.

Series D and E+: Preparing for the Endgame

- Series D: Typically 50–150 million+ at 700 million–2 billion+ valuations, used to strengthen the balance sheet for IPO or major acquisitions.

- Series E and beyond: Often 50–500 million+ at 1 billion+ valuations, reserved for mature “unicorn” companies closing the final gap to an IPO or very large sale.

In these rounds, investors will demand multi-year, predictable performance and public-market-ready operations. As your advisor, the conversation becomes less about product and more about capital structure, timing, and positioning for the public markets.

Benchmarks by Stage: What You Should Aim For

Use the following as directional targets, not rigid rules. They will help you calibrate both your valuation expectations and your internal growth plan.

- Pre-Seed: Typically pre-revenue, but must show a credible MVP, strong team, and clear early validation. Valuations often fall between 1–7.5 million, with many clustering around 5–6 million.

- Seed: Aim for 300k–500k ARR or strong leading indicators of revenue; valuations usually in the 10–30 million range, with many deals around 12–15 million.

- Series A: Target 1–3 million in ARR (sometimes 2–5 million), 15–20% month-on-month growth, and strong unit economics; valuations often 25–50 million, with many between 40–45 million.

- Series B: Typically 5–10 million ARR (up to 10–20 million for emerging leaders), with valuations in the 50–140 million range; recent medians have been around 100+ million.

- Series C: Often 20–50 million+ in ARR, with valuations starting around 100 million and extending to 500 million+.

- Series D+: Tens of millions (50–100 million+) in predictable ARR and valuations of 700 million to several billion, especially for pre-IPO rounds.