For decades, the US dollar has been the unquestioned backbone of global trade, reserves, and cross‑border capital flows. That dominance has not disappeared overnight – the dollar still clears most global transactions and anchors the deepest capital markets.

But beneath the surface, the direction of change is becoming harder to ignore, as more countries and institutions look for insurance against over‑reliance on a single currency and system.

Download Full Report: https://zfrmz.com/tFnQlpEkHilOFpGPB5uA

A quieter shift is already underway:

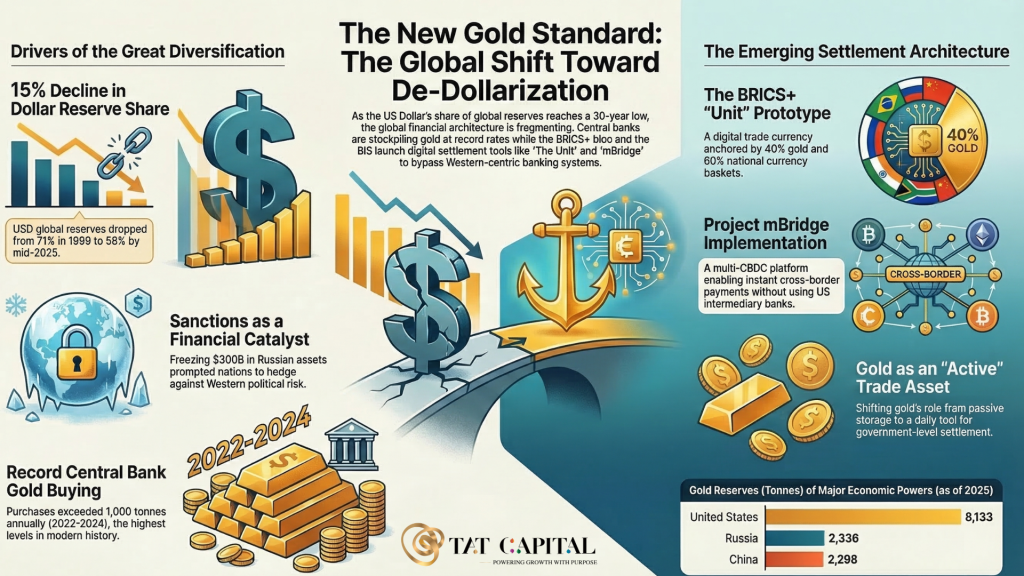

- Central banks are buying gold at record levels, adding more than 1,000 tonnes a year for several years running, signalling a renewed search for neutral, non‑sovereign reserves.

- Countries are actively testing non‑dollar trade routes, from local‑currency settlement in BRICS trade to bilateral deals that bypass traditional dollar funding.

- New settlement systems are emerging outside legacy rails like SWIFT, including experimental BRICS payment infrastructures and digital platforms designed for local‑currency and tokenised settlement.

- And businesses are waking up to a new reality — currency risk is no longer operational background noise, but a strategic lever that can reshape margins, cash flows, pricing power, and competitive position in global markets.

- This isn’t dramatic “sudden de‑dollarisation.” There is no cliff‑edge collapse or overnight replacement of the dollar. Instead, we are watching something more gradual but potentially more powerful: a multi‑year shift toward resilience, monetary sovereignty, and diversification of both reserves and payment rails.

In this report, we will break down:

- What’s really driving the incremental shift away from exclusive dollar dependence – from geopolitics and sanctions risk to reserve diversification and regional trade blocs.

- Why gold is quietly regaining importance as a reserve asset, with central banks using it as a long‑duration hedge against currency debasement and financial system shocks.

- How the BRICS framework and similar regional initiatives could reshape global trade flows by expanding local‑currency settlement and creating parallel payment infrastructures.

- And why FX risk management is becoming a core business capability, on par with capital allocation and pricing strategy, as firms look to protect margins, stabilise cash flows, and support long‑term planning.

The key takeaway: This is no longer a simple “USD vs Gold” world. It is a more complex system in which:

- The USD remains dominant and indispensable, especially for deep liquidity and global funding.

- Gold anchors trust in reserves, acting as a neutral store of value across political cycles and currency regimes.

- Multiple currencies and settlement systems coexist, from local‑currency trade within blocs like BRICS to new digital and token‑based rails that sit alongside traditional infrastructure.

And in that world, how you manage currency risk may matter as much as how you grow – because the firms that actively hedge, price, and structure around FX will not just survive volatility, they will use it to reinforce their strategic advantage.